The delayed pain of credit debt

Lesson 4

Today’s credit landscape is highly accessible, particularly for young people just starting out. Credit cards, store credit, Buy Now, Pay Later (BNPL) apps, and online payment options have made borrowing almost effortless, providing quick access to goods and experiences that might otherwise be out of reach. While these services bring convenience, they also heighten the risk of falling into debt traps, especially for those still developing financial management skills.

A key challenge is that credit creates an illusion of affordability and enhanced purchasing power by breaking down costs into smaller, manageable instalments over several months. This impression of readily available credit and the convenience of delayed payment often leads to overspending. Young people, in particular, may find it difficult to track or control their expenditures, which can result in cumulative debts that quickly become overwhelming.

Without careful financial planning, this cycle of easy credit can lead to significant debt accumulation. Over time, interest builds, payments add up, and young people who once enjoyed the freedom of credit may feel trapped by their financial obligations. Many end up making only minimum payments, which prolongs the repayment timeline and increases the overall amount owed.

There are two primary emotional drivers that contribute to why many individuals fall into the credit debt trap:

1) Instant Gratification: In our fast-paced world, the desire for immediate satisfaction is stronger than ever. We often want that new gadget, trendy outfit, or dining experience right away, and credit makes it all too easy to acquire these items without the need to save first. This impulsive behaviour can lead to a cycle of spending that prioritises short-term pleasure over long-term financial health. The thrill of making a purchase instantly satisfies our cravings, but this fleeting joy can quickly turn into regret once the bills arrive.

2) Peer Pressure: The influence of social circles cannot be underestimated. We feel a strong urge to keep up with our friends’ spending habits, leading to unnecessary purchases driven by the need for social acceptance or status. This phenomenon, known as social comparison, can encourage us to spend beyond our means, as we often equate our worth with our ability to consume. When we see our peers flaunting the latest trends or experiences, we may feel compelled to follow suit, even if it means taking on debt. This pressure can create a toxic cycle where we sacrifice our financial stability for the sake of fitting in or maintaining a certain image.

These emotional factors, combined with the ease of access to credit, create a perfect storm that can lead to overspending and mounting debt.

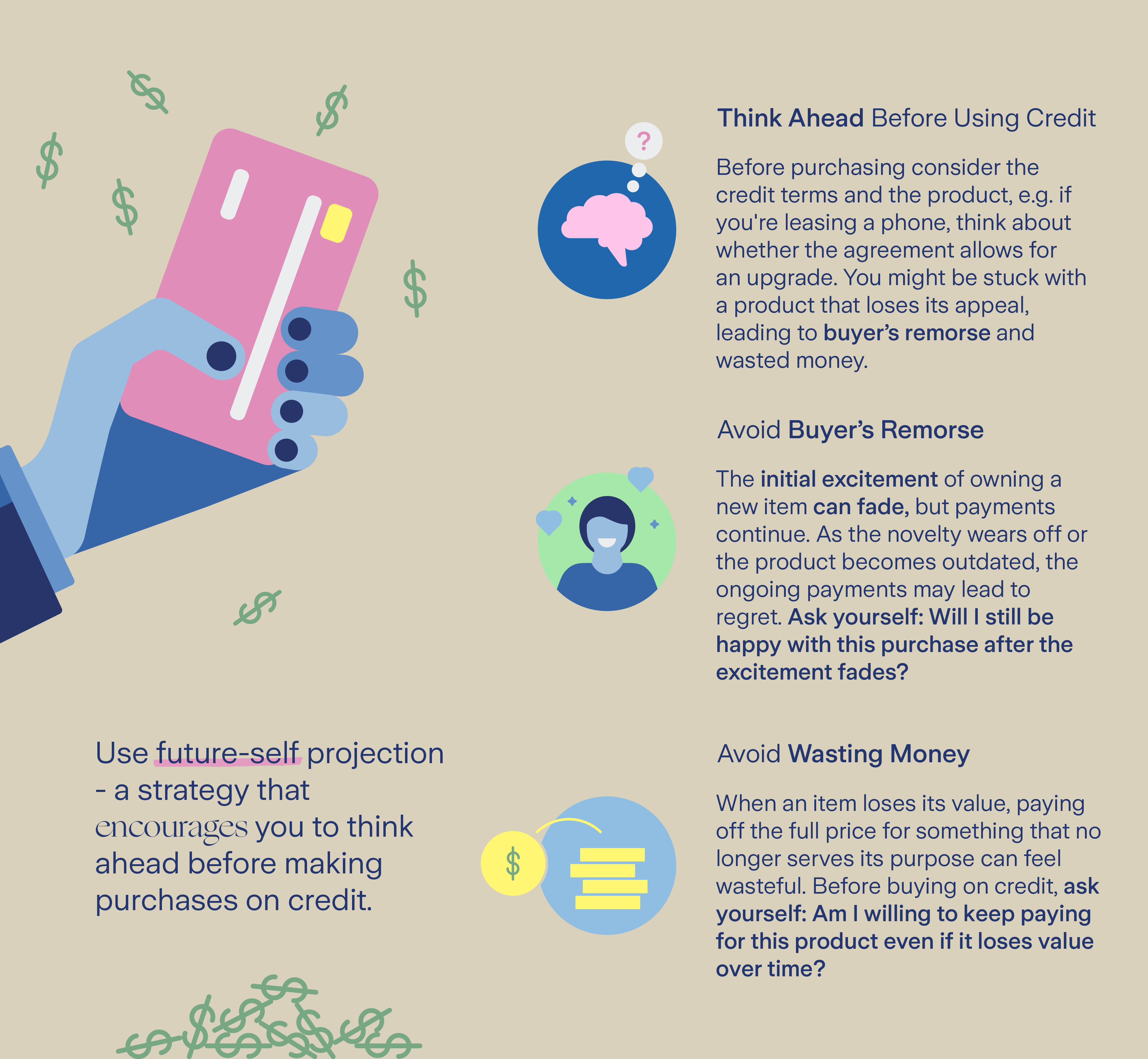

To curb impulsive spending and avoid falling into the traps of credit debt, it's essential to think ahead. Future-self projection is a valuable strategy that empowers you to avoid debt and make informed financial decisions that prioritise long-term wellbeing over instant gratification or social conformity. Take a moment to project yourself into the future and consider the potential delayed pain that may arise from accumulating credit debt.

Before making a purchase on credit, take a moment to think about the future and evaluate both the credit terms and the product. For instance, if you’re leasing a mobile phone, consider whether the agreement allows for an upgrade to a newer model. Without this option, you could find yourself stuck with two common psychological traps:

1) Buyer’s Remorse: Imagine the excitement of owning a new phone fades after just a few months, but the bills keep coming. You bought the latest smartphone on credit, with payments spread over two or three years. While the initial thrill and boost in status feel great, the device soon starts to show signs of wear and tear. As time passes, it loses its novelty, and you may even find yourself dreaming about replacing it. If its performance declines or it gets damaged within a year, you’re stuck making payments for something that no longer meets your expectations. When the initial excitement fades but the payments continue, regret and guilt can set in. The longer the repayment period, the more uncomfortable those payments feel. This phenomenon is known as the "pain of paying", and it can lead to significant buyer’s remorse. To prevent this, ask yourself first: Will I still feel good about this purchase once the novelty wears off?

2) Wasting Money: Consider what happens when an item loses value, like a smartphone that becomes outdated or gets stolen. Paying full price for something that no longer serves its purpose can feel like throwing money away. What started as an investment in something valuable becomes a burdensome financial obligation. The ongoing repayments overshadow the initial excitement of owning the product, leaving you with a sense of wastefulness and financial loss. Before buying on credit, ask yourself: Am I prepared to keep paying for this product even if it loses its value over time?

By projecting yourself into your future self dealing with credit repayments, you can equip yourself with the tools to overcome instant gratification and peer pressure. First, it allows you to understand the relationship between the value of credit and the worthiness of the product. Secondly, imagining your future helps you realise that the thrill of gratification may last only a few months. Developing a forward-thinking mindset enables you to weigh the long-term implications of your credit choices, fostering healthier financial decisions that prioritise credit use only when it is truly necessary.