State pensions may not exist when you want to retire

RiskArticleOctober 30, 2020

As it becomes increasingly hard for some nations to afford state pensions, Zurich Insurance Group (Zurich) and VICE look at what this means for us and our future

Are you expecting to get a state pension when you retire, with a similar amount to what your parents or grandparents were able to get? Because if you are a millennial or younger you should be thinking that state pensions might not exist when you want to retire in thirty to forty years. It will become increasingly hard for some nations to afford these, with people living longer than ever before and not having as many children as they once did. These demographic changes mean there are going to be less people working and more people claiming pensions, which means governments are going to be making difficult decisions.

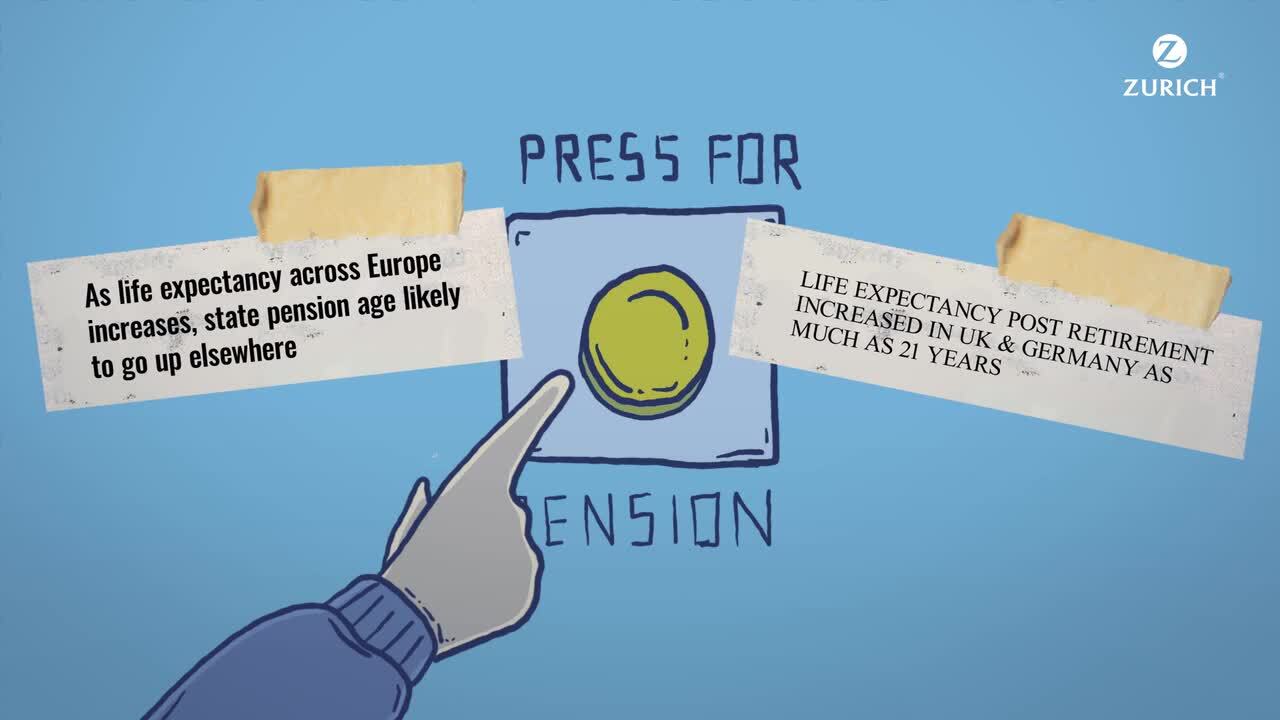

In the UK, the government started to gradually raise the age at which people become eligible for the state pension from 65 to eventually reach 68. There are plans to make further changes over the coming years according to the Pensions Advisory Service. With life expectancy across Europe increasing, it is likely the state pension age will go up elsewhere.

Professor Gordon Clark, Professorial Fellow at Oxford University, told VICE: “Retiring at 63/65 is not consistent with the system. A 65 year old now is a lot healthier than what they were 25 years ago. People are living longer. 25 years ago the average male could expect to live to 78/79, now they can expect to live to 83/85.”

This is in part because the system of state pensions was not designed for the modern era, or for the purposes we think of them now. Dr Stefan Kroepfl, head of life planning and development for Zurich Insurance Group (Zurich), said: “When the pension system was introduced in Germany in 1890, the pension age was the same as it is today, it was 70. The average life expectancy back then in Germany was actually much lower. Now, that didn’t mean nobody got a pension, but it meant many people died before they got a pension. Those who lived long enough to enjoy a state pension on average, were living for another seven/eight years.”

The amount of time we are now living after retiring has more than doubled, according to Kroepfl, who added: “Today, the life expectancy in Germany after you retire, and it's fairly similar in the UK, is another 17-18 years for males and for females, it even is around 21 years”

While women might be living longer, they are at a greater risk than men of facing problems when they come to retire. Particularly if they take breaks from employment to have or care for children. Clark warned: “Lots of evidence suggests they are the losers in this type of system, relative to men who stay employed or in the workplace through their entire lives. You have to look at the equitability of these kinds of systems, male to female, over the long term, because it is quite clear that, on average, women with the same income starting out, basically end up with a lot lower workplace pension benefit.”

There are only a handful of ways we can address the problems with state pensions according to Kroepfl, who said: “You can either increase the contribution, so the amount of money you will pay in while you are working. Or you can decrease the pension payment, the amount of money you get out. There is one more thing you can do in order to stabilize the system. That is increase the pension age.”

Increasing the pension age means those of us who have not retired yet will have to work for longer, but this does not necessarily mean we will be doing the same jobs we are now or working anywhere near as much, once we get older. Clark added: “People's adaptiveness has improved over time. People are healthier, they do very different jobs they did 35 years ago, less physically demanding, more a mental kind of productivity.”

While our jobs might be getting easier to do, we still need to be thinking about how we are planning on retiring, if we are ever able to make it happen. Kroepfl warns: “The state pension might not exist, at least not in the shape, or form that we have them today. The one thing which I think is the least likely is that the contribution payments will increase. If young people or workers today want to retire at a younger age, or they want to retire at a higher standard of living, they need to pay the contributions themselves. It is strikingly clear to me.”

But it is not all bad. Kroepfl adds: “The only other thing I can offer to help solve the problem is, one of the assets that you have from your youth: time. When you save for retirement, even small amounts of money invested regularly can grow quite big. If you are able to do that over 30-40 years, then that will be a nice pension. If you're struggling, start with a small amount, but do it regularly and never stop.”