With disruption comes opportunity

Global risksArticleOctober 8, 20205 min read

‘The world is more challenged than ever, says Guy Miller, Chief Market Strategist, Head of Macroeconomics, but the current upheavals, risks and disruptions must be seen as creating the catalyst and opportunities for change.’

2020 was never going to be an easy year. Increasing geopolitical skirmishes and rising social tensions around inequality came on top of dramatic climate related events and the disruptive impact of the fourth industrial revolution. Little did we know, back at the start of the year, that a global pandemic and depressionary economic conditions would be added to the challenges that we faced.

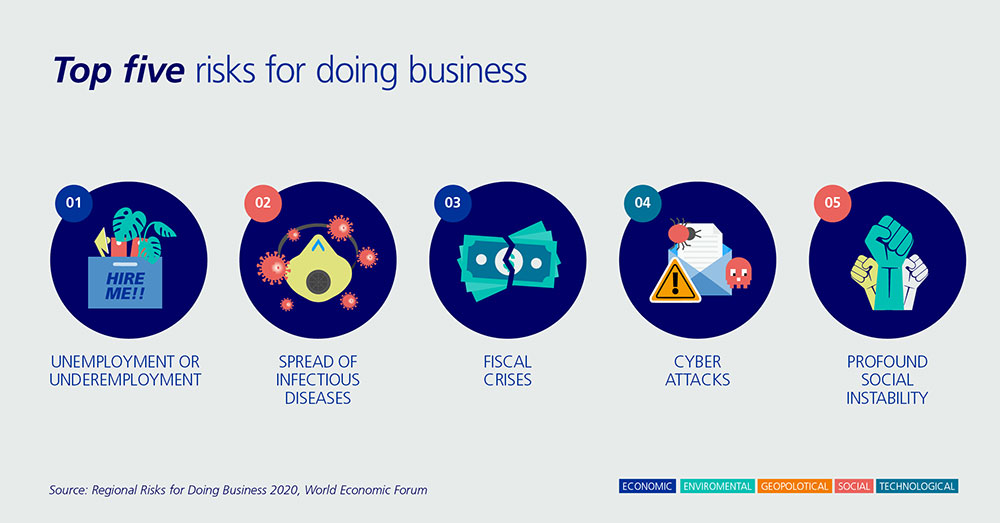

In the latest Risks for Doing Business report, produced by the WEF in collaboration with Zurich Insurance Group, there was no shortage of topics to include. It wasn’t surprising that ‘Spread of Infectious Disease’ surged to the number two spot in the global survey of business leaders, with Unemployment remaining on top again this year, and Fiscal Crises rounding off the top three rankings.

While Profound Social Instability and Asset Bubbles moved up within the top 10, the immediacy of the current health and economic crisis perhaps explains why no environmental risks made it into the top 10, despite gaining impetus. This, to me, however, under-represents the potential severity, frequency and protracted nature of this category.

It certainly feels as though the world is more challenged than ever. In addition to the profound tectonic shifts created around climate and technological change, the first pandemic in a hundred years resulted in a global recession, as economies were deliberately shut in a bid to contain the spread of the virus. Meanwhile, the fiscal and monetary spigots were opened to preserve productive capacity and prevent the health and economic crises also manifesting into a financial market crisis.

On this front at least, credit is due as the global response was quick and decisive. However, the pandemic has highlighted weaknesses in most healthcare systems, where years of complacency and underinvestment have been exposed, with the resulting economic and societal cost to contain the virus a much-needed wake up call.

Opportunity for change

As we take stock of the most pressing risks, they need to be viewed as an opportunity for change. Many are integrated with mutual dependencies and commonalities that often stem from a lack of sustainable economic expansion. What is clear to me, is that the quest for cleaner, more balanced, equitable and dynamic growth must be hastened if the risks and their consequences are to be mitigated.

The closing down of economies also highlighted inequalities between countries. As governments have tried to keep productive capacity of their economies intact, the cost of providing worker protection in a variety of schemes has soared. In the US, the unemployment rate went from a 60-year low of 3.5% in February, to a record high of 14.7% by April, with around a quarter of the working population being impacted in some form.

Fiscal deficits as a share of GDP have hit double digits in many regions, from Japan and Singapore, to the Eurozone, Brazil and the US. Record levels of government debt in both developed and emerging economies have surged ever higher. While funding costs are exceptionally low, making this manageable in the short term, there is a fiscal vulnerability that is building.

Investing in the long-term

Of course, government spending is required to support the labor market and keep the fabric of societies functioning in such times of crisis, but there is a need to make sure that spending is also in the form of long-term investment to achieve that transition to a better form of growth.

In this regard, the European Union’s repair and recovery fund is encouraging. The €750 bn grant and loan facility, representing more than 5% of the EU’s GDP, is trying to catalyze sustainable growth in a bid to stimulate private sector investment and ultimately reposition the competitiveness of its member countries. While many hurdles lie ahead and the scale is still somewhat modest, it is a profound step for the region and one which hopefully others will follow. If not, it is hard to see how higher and more sustainable growth can be achieved.

Existing policies of increased spending by governments to plug gaps and broadening asset purchase by central banks only works up to a point and does not address the underlying cause of many of the problems – and can even generate others. Indeed, while the midst of a pandemic does not seem the right moment to be worrying about asset bubbles, the liquidity-induced new records being set by stock markets suggest the disconnect between financial assets and the real economy is a legitimate concern.

With interest rates having hit the lower bound in many regions, central bank balance sheets have ballooned – by the tune of around USD6 trillion this year alone – as asset purchase have become the primary tool of monetary policy. While I applaud the intent of the action so far to avoid a financial crisis coming on top of everything else, unless monetary and fiscal policies are overhauled and underlying growth is regenerated, we may yet have to face the crisis that is waiting in the wings.

Perhaps every generation feels that the outlook is particularly challenged, but the current upheavals, risks and disruptions must be seen as creating the catalyst and opportunities for change.

Blog from Guy Miller, Chief Market Strategist, Head of Macroeconomics.