Three ways insurers can support business in their climate change strategies

Climate resilienceArticleSeptember 26, 2023

The impact of climate change is becoming more evident every year. Companies must embrace the net-zero transition – and fast. How can the insurance sector help?

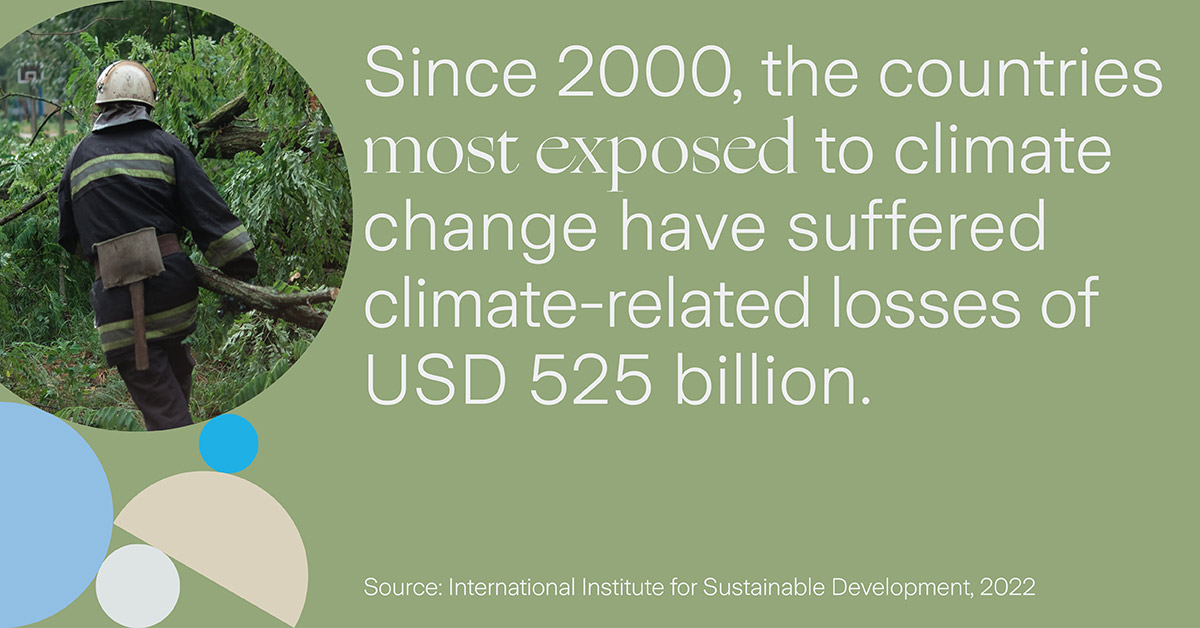

Climate change is taking a heavy toll not just environmentally and financially but on society as well. Since 2000, the countries most exposed to climate change have suffered climate-related losses of USD525 billion. The ripple effects of rising temperatures and catastrophes at regional level spread through businesses, disrupting supply chains, inflicting damage to property, raising operating costs and affecting employee well-being.

Related download

In response, companies have recognized the urgent need to transition to net-zero. In 2022, a remarkable 42 percent of Fortune 500 companies had already laid out comprehensive net-zero strategies, a significant rise from the preceding year’s 31 percent. Commitments have reached national levels, as 140 nations contemplate or declare their net-zero strategies.

Looking at how to build a greener future, Zurich surveyed over 650 sustainability leads across 15 countries to find out more about how companies are approaching the transition to net-zero in the next three to five years. What are the challenges? What are the opportunities? And what needs to be the priority to speed up progress?

The state of transition

Seventy-seven percent of companies surveyed had a net-zero plan. Within these organizations, it’s noteworthy that investors and managers wield the most significant influence in advocating for net-zero actions, surpassing the impact of customers, regulators and media.

The main hurdles in their climate transition plans include: the substantial costs involved (50 percent); technological limitations (46 percent); regulatory complexities (44 percent); challenges in effectively monitoring impact (44 percent); a shortage of essential skills (35 percent); the intricacies of balancing short-term priorities (30 percent); securing access to necessary finance (30 percent); concerns about potential impacts on competitiveness (25 percent); and the task of garnering internal support (24 percent).

These are complex challenges, and no one business – or even industry – can effectively address them all alone. Meaningful climate transition calls for a cross-sector approach with considerable work within companies themselves, alongside wider society, regulatory bodies and academic institutions.

The role of the insurance sector

Global progress toward achieving net-zero targets remains sluggish, partly because of the complexity involved and a lack of coordination in mitigation efforts. Based on current trends, temperatures could increase by more than 1.5ºC by 2040. The seemingly incremental change would have devastating effects. Extreme heat waves, floods and droughts would become even more frequent, impacting local communities, critical infrastructure and global food supplies as well as triggering mass migration both across borders and within countries. For businesses, extreme weather events can disrupt global supply chains and reduce the availability of certain materials when areas of production are affected.

Our survey highlighted how the insurance sector has a vital role to play in sharing expertise, acting as a knowledge hub and coordinating efforts between stakeholders to cope with the immediate effects of climate change. Given the challenges and opportunities businesses face in the coming years, here are three ways insurers can help adapt to climate change:

- Risk Assessment: Prevention is better than a cure, and investment in adaptation and mitigation has much more potential for impact. Yet there’s a huge finance gap. In developing countries, the cost of adaptation is estimated to be five to 10 times higher than the amount that has been earmarked to complete it. As experts in risk assessments, the insurance sector can take a data-led approach by combining business and climate data to increase resilience across an organization’s value chain. Insurers can also coordinate between new tech, academia, policymakers and local governments to develop effective mitigation strategies. Company leaders can’t plan for the future if they’re struggling to survive the present, and solutions necessitate involvement of all stakeholders due to the complexity of the risks.

- Resilience: With extensive experience understanding vulnerabilities, risk timelines and the value of investments, the insurance sector is well positioned to help design adaptation strategies and implement mitigation strategies in a way that does not increase risk.

- Recovery: In instances where damage can’t be avoided, the insurance sector will be key in helping businesses recover from shocks or disasters and rebuild stronger than before. Post-event recovery assistance will be vital in the coming years as our environment evolves alongside the changing climate. With networks that have taken decades to cultivate, insurers can build recovery coalitions among policyholders, authorities and communities – literally “building back better.”

Governments, companies and citizens all have a role in successfully steering businesses to net-zero. The insurance sector can be an architect of change by helping direct investment toward effective sustainability efforts and aiding recovery in places affected by climate change. By supporting the global transition to sustainability, the insurance sector can be a powerful agent in building a greener future.

Climate Resilience

Our Climate Resilience experts help you identify and manage climate risks, and prepare you for climate reporting.